Published: September 2025

Here's a sobering statistic: Over 40% of Australian small business failures in 2023-24 listed cash flow shortages as a contributing factor, according to ASIC data. These weren't unprofitable businesses - they were companies that simply couldn't convert their paper profits into cash when they needed it most.

The culprit? Poor cash flow forecasting. Or more often, no forecasting at all.

Your profit and loss statement tells you what happened last month. A cash flow forecast tells you whether you can make payroll next week. In the unforgiving world of Australian small business - where the ATO doesn't negotiate and suppliers demand payment—that difference can make or break your company.

Think of cash flow forecasting as your business's GPS. Without it, you're driving blind through the financial landscape, hoping you don't hit a wall.

The Timing Trap

Consider this common scenario:

Your July P&L shows a healthy profit. Your bank account shows a different story entirely.

The Australian Context

Running an SME in Australia comes with unique cash flow challenges:

A proper forecast doesn't just predict these cycles - it helps you survive them.

Strip away the complexity, and every cash flow forecast has three moving parts:

The magic formula: Closing Balance = Opening Balance + Inflows - Outflows

Simple? Yes. Effective? Absolutely - if you get the details right.

For tight cash situations: Weekly forecasts for 13 weeks

For strategic planning: Monthly forecasts for 12-18 months

Best practice: Rolling 13-week weekly forecast with monthly extensions

You'll need:

Customer receipts: Don't count invoices, count cash. If your average debtor days are 45, only 60% of this month's sales will convert to cash this month.

Example breakdown:

Other inflows: ATO refunds, grants, equipment sales, capital injections

Operating expenses:

Supplier payments:

Government obligations:

Other outflows:

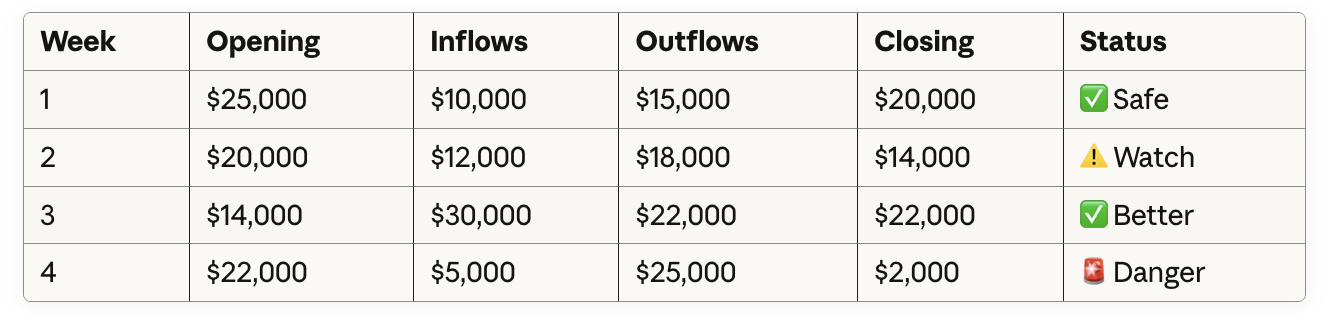

Week 1 example:

That negative $15,000 is your early warning system.

Build your forecast forward 13 weeks. Update it weekly with actual results. The magic happens when you consistently compare forecast vs. actual and adjust your assumptions.

Week 4 shows a critical cash shortage. Without this forecast, you'd discover it when payroll bounces.

- Debtor management: Identify which overdue invoices threaten next week's payroll

- Supplier negotiations: Extend payment terms when you see tight periods coming

- ATO planning: Set up payment plans before you're in breach

- Investment timing: Test scenarios before hiring staff or buying equipment

- Banking relationships: Show lenders you manage cash proactively

Q: Cash basis or accrual basis?

Always cash. You're tracking bank movements, not accounting profits.

Q: How far ahead should I forecast?

13 weeks for operations, 12 months for strategic planning.

Q: Should I use software or spreadsheets?

Both work. Xero add-ons like Fathom automate updates, but spreadsheets build discipline.

Q: How accurate should my forecast be?

Aim for 80% accuracy on the first month, 60% on the third month. Perfection isn't the goal—early warning is.

Start simple. Build a 4-week forecast using last month's bank statement as your guide. Update it weekly. Once you see the power of forward visibility, extend it to 13 weeks.

Remember: The best forecast is the one you actually use.

Scale Suite is a Sydney-based provider of outsourced finance teams and fractional CFO services for Australian SMEs. We deliver weekly bookkeeping, payroll, BAS/IAS lodgement, cashflow reporting, management accounts, and strategic fractional CFO oversight - all as a fully embedded team that works inside your business.

CA-qualified, Xero Certified, and registered BAS Agents, we replace fragmented bookkeepers and once-a-year accountants with one responsive finance function at a fraction of the cost of full-time hires. We serve growing businesses across Sydney, Melbourne, Brisbane, and Perth, with packages starting from $1,500 per month and no lock-in contracts.

Learn more about our embedded finance model at scalesuite.com.au/services/finance

Scale Suite is a Sydney-based provider of outsourced finance and HR services for Australian SMEs. We deliver bookkeeping, financial reporting, payroll processing, fractional CFO support, recruitment, employee onboarding, people and culture support, and fractional HR oversight, all as a fully embedded team that works inside your business.

Employment Hero Gold Partner, CA-qualified, and Xero Certified, we replace fragmented finance and HR processes with one responsive, senior-level function at a fraction of the cost of full-time hires. We serve growing businesses across Sydney, Melbourne, Brisbane, and Perth, with packages starting from $1,500 per month and no lock-in contracts.

30 minutes with our team.

We'll review your current finance setup, compare the full cost of an internal hire against our embedded team, and show you exactly what your finance function should cost at your stage of growth.

You'll leave with a clear view of what's working, what's missing, and where you'd save.

No lock-in contracts. 30-day money-back guarantee.

Prefer to book directly? Grab a time here.