Published: October 2025

When starting or restructuring a business in Australia, selecting the right legal structure is crucial. It affects taxation, liability, asset protection, and growth potential. Two common options are trusts and companies. This article explores the key differences, advantages, and disadvantages to help you decide. Remember, every business is unique, so professional advice is essential.

Your choice of structure influences how income is taxed, how assets are protected, and how easily you can raise capital. For instance, trusts often provide flexibility in distributing income, while companies offer a more formal framework suitable for expansion. According to the Australian Taxation Office (ATO), the structure must align with your business goals, and changes can involve costs like stamp duty or capital gains tax.

A company is a separate legal entity under the Corporations Act 2001, registered with the Australian Securities and Investments Commission (ASIC). It can own property, enter contracts, and incur debts independently of its owners. Ownership is through shares, and management is typically handled by directors.

A trust is not a separate legal entity but an arrangement where a trustee holds assets for beneficiaries, governed by a trust deed. Common types include discretionary trusts (flexible distributions) and unit trusts (fixed units like shares). Trusts are popular for family businesses and must distribute income annually.

Most business owners setting up a discretionary trust are advised to use a company as the trustee rather than acting as trustee personally. This is called a corporate trustee structure and it is the standard recommended approach for any business trust.

With a personal trustee, if you are sued personally, your assets as trustee may be at risk even where those assets are held on behalf of beneficiaries. A corporate trustee creates a separation - the company is the trustee, not you personally. This significantly strengthens the asset protection the trust structure provides.

The practical setup is: you establish a company (often with a name like "Smith Family Pty Ltd" or "[Business Name] Trustee Pty Ltd"), and that company acts as trustee for your discretionary trust. You and your spouse or family members are directors and shareholders of the trustee company. The trust deed specifies who the beneficiaries are.

This structure adds one layer of setup cost (ASIC registration for the trustee company, a small annual review fee) but the asset protection benefit generally justifies it. Most solicitors and accountants recommend this approach as standard for any business discretionary trust.

The hybrid structure: trust plus operating company

A common configuration for established Australian businesses combines both structures:

This structure aims to capture the company's lower tax rate on retained profits while preserving the trust's flexibility in distributing franked dividends to beneficiaries. It adds complexity and compliance cost but can be highly tax-effective for profitable businesses.

The right structure depends on your specific circumstances, profit levels, beneficiary tax positions, and long-term goals. This is exactly the kind of decision where professional advice from an accountant or solicitor pays for itself many times over.

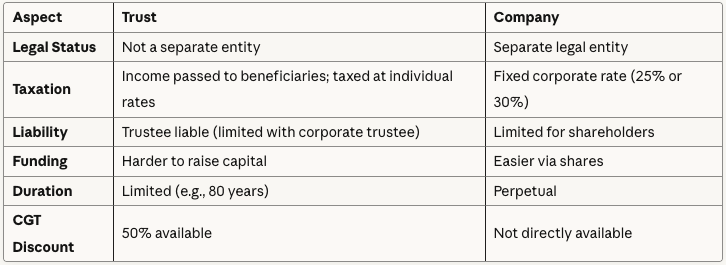

To compare, consider these aspects:

Trusts suit businesses focused on tax minimisation and family involvement, while companies are ideal for scaling and external investment.

Understanding the conceptual differences between trusts and companies is useful. Seeing the dollar impact is more useful.

Example 1: Retaining profits in the business

A Sydney technology services business generates $300,000 in taxable profit. The owner wants to retain most of this profit in the business for reinvestment.

Under a company structure (base rate entity at 25%): tax of $75,000. Net retained: $225,000.

Under a discretionary trust: the trust must distribute all income. If the owner takes the full $300,000 personally (assuming no other beneficiaries in lower tax brackets), at a marginal rate of 37% plus Medicare levy they pay approximately $114,000 in tax. Net received: $186,000.

Advantage: company structure by $39,000 for profit retention.

Example 2: Income splitting with family beneficiaries

The same business generates $300,000. The owner has a spouse earning $40,000 from other sources and two adult children earning $20,000 each from part-time work.

Under a company structure: $75,000 in company tax. To extract money, the owner pays a salary or dividend (franked at 25%), which attracts further tax at personal rates.

Under a discretionary trust: the trustee distributes $80,000 to each beneficiary. The spouse's taxable income becomes $120,000 - tax of approximately $28,800 plus Medicare. Each adult child's income becomes $100,000 - tax of approximately $22,800 plus Medicare each. Total family tax: approximately $74,400.

Advantage: trust structure by approximately $600, plus the family retains the cash directly rather than it sitting in a company.

Example 3: Selling a business asset

The business sells a piece of equipment held for three years for a $200,000 capital gain.

Under a company structure: capital gain of $200,000 taxed at 25% corporate rate = $50,000 tax. No 50% CGT discount applies to companies.

Under a trust: capital gain of $200,000, with the 50% CGT discount the taxable gain is $100,000. Distributed to a beneficiary at 37% marginal rate = $37,000 tax.

Advantage: trust structure by $13,000 on this transaction.

These examples illustrate why the right structure depends on what you are optimising for - profit retention, income splitting, or asset realisation. No single structure wins across all scenarios.

The choice of structure directly affects your ongoing bookkeeping and accounting obligations, which have a real cost.

Company bookkeeping and compliance:

Trust bookkeeping and compliance:

Common mistakes to avoid:

Failing to make the annual trustee resolution before 30 June is one of the most expensive and easily avoided tax mistakes a trust can make. The resolution determines how income is distributed to beneficiaries for that financial year. Without it, the default position under most trust deeds is that income accumulates in the trust and is taxed at the top marginal rate of 45%.

Family trust elections are irrevocable elections that determine who qualifies as a family member of the trust for the purposes of loss transfer and franking credit streaming. Once made, they cannot be changed. They can also make it harder to add new beneficiaries later. This is another area where professional advice before making the election is essential.

At Scale Suite we work with clients operating under both structures and handle the bookkeeping, payroll, BAS, and reporting obligations that each requires. See our complete guide to outsourcing bookkeeping in Australia for how outsourced bookkeeping works across different business structures.

Decide based on your needs: opt for a trust if flexibility and protection are priorities, or a company for stability and growth. Review your structure regularly, as business changes may warrant a switch. Always seek expert guidance to navigate ATO rules and avoid pitfalls like family trust elections or public trading trust issues.

Business circumstances change and the structure that made sense when you started may not be optimal five years later. Common triggers for reviewing your structure include:

From sole trader to trust or company: When your business becomes profitable enough that personal tax rates are a significant burden, when you want to bring in business partners, or when liability exposure makes personal trading risky.

From company to trust-plus-company hybrid: When you want to introduce family members as beneficiaries for income splitting purposes, or when you have significant assets you want to separate from the operating business for protection purposes.

From trust to company: When you need to raise external capital from investors (trusts can be restrictive for third-party equity), when you are preparing for an exit or trade sale (companies are generally cleaner to sell), or when the complexity and compliance cost of the trust structure no longer justifies its benefits.

The cost of changing: Restructuring is not free. Transferring assets between structures can trigger capital gains tax and stamp duty depending on your state. The ATO also has specific rules about restructuring and small business rollovers that may apply. A restructure done properly with professional advice can be highly tax-effective. A restructure done without advice can generate an unexpected tax bill.

Our article on company structure vs sole trader in Australia covers the earlier stage decision between these options for newer businesses.

What is the main difference between a trust and a company in Australia?

A company is a separate legal entity under the Corporations Act 2001 - it can own property, incur debts, and enter contracts in its own name. It pays tax at a flat corporate rate of 25% or 30%. A trust is not a separate legal entity. It is an arrangement where a trustee holds assets for the benefit of beneficiaries. Trusts must distribute income annually to beneficiaries who are then taxed at their own marginal rates. Companies retain profits; trusts distribute them.

When should I choose a trust over a company?

A discretionary trust is generally more suitable when income splitting with family members in lower tax brackets is a priority, when you want the 50% CGT discount on business assets held for more than 12 months, when privacy is important (trust beneficiaries are not publicly disclosed), and when the business is family-operated with no plans for external investment. A company is generally more suitable when you want to retain profits in the business at the lower corporate rate, when you plan to raise capital from investors, or when you are preparing for a trade sale or IPO.

What is a corporate trustee and why is it recommended?

A corporate trustee is a company that acts as trustee for a trust rather than an individual. It is the standard recommended structure because it provides stronger asset protection -- the trustee company's liability is separate from your personal liability. Without a corporate trustee, your personal assets as trustee may be exposed in certain circumstances. The additional setup and annual compliance cost is typically modest relative to the protection benefit.

What happens if a trust doesn't distribute all its income by 30 June?

Undistributed income is taxed at the top marginal rate of 45%, plus the Medicare levy. This is one of the most important compliance deadlines for any trust. The annual trustee resolution distributing income must be made and documented before 30 June each year. Missing it, or failing to document it properly, can result in a substantial unnecessary tax liability that cannot be retrospectively corrected.

Can I change from a trust to a company later?

Yes, but the restructure may trigger capital gains tax on assets transferred, stamp duty in some states, and a range of other tax considerations. The ATO has small business restructure rollover provisions that can defer these taxes in some circumstances, but the rules are complex. Always obtain professional advice before restructuring - a well-planned restructure can be highly tax-effective while a poorly planned one can be expensive.

Is a trust or company better for asset protection?

Both provide some protection but through different mechanisms. A company protects shareholders' personal assets from company debts (provided the company is properly managed and directors avoid misconduct). A trust provides protection because beneficiaries do not directly own the trust assets - a personal creditor of a beneficiary generally cannot access trust assets. Using a corporate trustee enhances trust asset protection further. For the strongest protection, many established businesses use a trust-plus-company structure where the operating company is owned by the trust.

How does GST apply to trusts and companies?

GST registration requirements and obligations are essentially the same for both structures. If annual turnover exceeds $75,000, the entity must register for GST and lodge BAS regardless of whether that entity is a company or a trust. The trustee of a trust registers the trust for GST, and the trust lodges its own BAS. See our BAS guide for full details.

What are the ongoing compliance costs for each structure?

For a company: ASIC annual review fee (currently $310), annual tax return preparation by an accountant (typically $1,500 to $4,000 for a small company), and any bookkeeping costs. For a trust: annual trustee resolution preparation, annual trust tax return (typically $1,000 to $2,500), beneficiary tax returns, and bookkeeping costs. If the trust uses a corporate trustee, add the company's ASIC fee and corporate compliance. Combined trust-plus-company structures are the most expensive to maintain but offer the greatest flexibility.

Scale Suite is a Sydney-based provider of outsourced finance teams and fractional CFO services for Australian SMEs. We deliver weekly bookkeeping, payroll, BAS/IAS lodgement, cashflow reporting, management accounts, and strategic fractional CFO oversight -- all as a fully embedded team that works inside your business.

CA-qualified, Xero Certified, and registered BAS Agents, we replace fragmented bookkeepers and once-a-year accountants with one responsive finance function at a fraction of the cost of full-time hires. We serve growing businesses across Sydney, Melbourne, Brisbane, and Perth, with packages starting from $1,500 per month and no lock-in contracts.

Learn more about our embedded finance model at scalesuite.com.au/services/finance

We review and check articles periodically. At time of writing, all information is accurate to the best of our knowledge. This article provides general information only and does not constitute legal, tax, or financial advice. Business structure decisions should be made with advice from a qualified accountant and solicitor specific to your circumstances.

Scale Suite is a Sydney-based provider of outsourced finance and HR services for Australian SMEs. We deliver bookkeeping, financial reporting, payroll processing, fractional CFO support, recruitment, employee onboarding, people and culture support, and fractional HR oversight, all as a fully embedded team that works inside your business.

Employment Hero Gold Partner, CA-qualified, and Xero Certified, we replace fragmented finance and HR processes with one responsive, senior-level function at a fraction of the cost of full-time hires. We serve growing businesses across Sydney, Melbourne, Brisbane, and Perth, with packages starting from $1,500 per month and no lock-in contracts.

30 minutes with our team.

We'll review your current finance setup, compare the full cost of an internal hire against our embedded team, and show you exactly what your finance function should cost at your stage of growth.

You'll leave with a clear view of what's working, what's missing, and where you'd save.

No lock-in contracts. 30-day money-back guarantee.

Prefer to book directly? Grab a time here.